Health

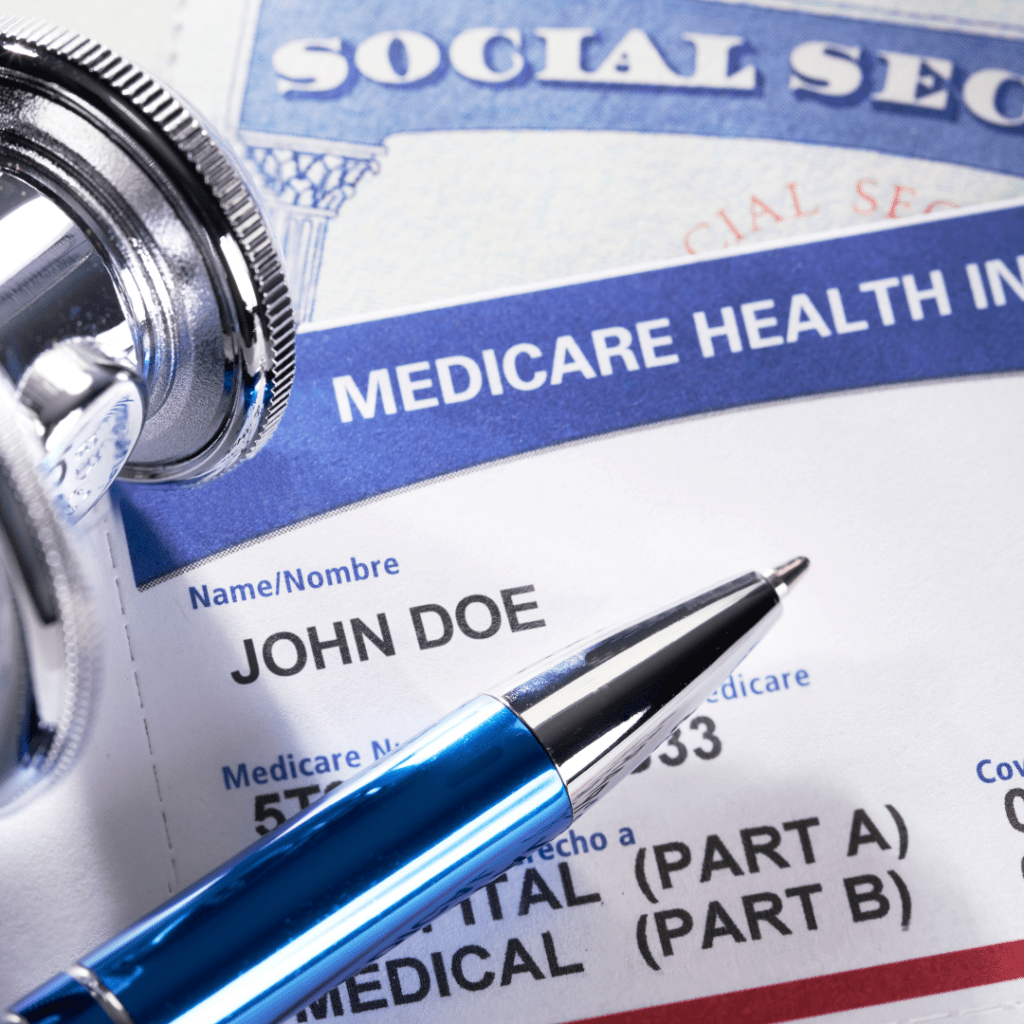

Social Security Benefits Expected to Increase in 2025: What You Need to Know

Social Security benefits are expected to increase by 2.57% in 2025 due to inflation. Learn about how the COLA works and its impact on retirees.

As inflation trends continue to influence the economy, Social Security benefits are projected to see a modest increase in 2025.

Current estimates suggest a 2.57% cost-of-living adjustment (COLA) for beneficiaries, which, while helpful, reflects a slowdown in inflation compared to recent years.

This potential adjustment has sparked interest among retirees and those nearing retirement, as they consider how these changes might impact their financial planning.

What to Expect from the 2025 Social Security COLA

The Senior Citizens League, a nonpartisan advocacy group, has estimated that Social Security benefits could rise by approximately 2.57% in 2025.

For the average Social Security recipient, who currently receives about $1,840 per month, this increase would translate to an additional $47 per month.

However, this amount could be reduced by potential increases in Medicare Part B premiums, which are expected to be announced later this year.

Compared to the 3.2% increase in 2024, this projected COLA is slightly lower, reflecting the cooling of inflation over the past year.

Despite this, the adjustment is still a vital mechanism for ensuring that the purchasing power of Social Security benefits keeps pace with the cost of living.

Understanding How COLA Works

One common misconception about the COLA is that it only benefits those who are already receiving Social Security benefits.

However, as Mary Johnson, an independent Social Security and Medicare policy analyst, explains, “The COLA should not be used to determine a retirement date at all because it is automatically factored into the benefit calculation used by Social Security.”

This means that even if you have not yet filed for Social Security benefits, as long as you are at least 62 years old in 2024, your future benefits will be adjusted for inflation, ensuring you receive the appropriate COLA increase when you eventually begin claiming benefits.

The Social Security Administration (SSA) confirms that those eligible for benefits starting at age 62 will see their benefits adjusted yearly based on the COLA.

Whether you claim your benefits at the earliest eligibility age, your full retirement age, or delay until age 70 to maximize your monthly payments, the COLA will be factored in.

The Role of Inflation in Determining COLA

The COLA is determined by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) for the third quarter of the current year to the same period in the previous year.

This formula means that the final COLA figure will be released in October, after inflation data for July, August, and September is fully analyzed.

Mark Zandi, chief economist at Moody’s, projects a 2.6% COLA increase for 2025, aligning closely with the Senior Citizens League’s estimate.

Zandi attributes the moderation in inflation to the easing of pandemic-related disruptions and other global economic factors that previously drove inflation higher.

The Financial Impact of COLA on Retirees

While the COLA is designed to help retirees keep up with rising costs, other factors may offset this benefit.

For instance, Medicare Part B premiums are automatically deducted from Social Security benefits, and any increase in these premiums will reduce the net gain from the COLA.

The Medicare Trustees have forecasted a rise in Part B premiums to $185 per month in 2025, up from $174.70 in 2024.

This increase could lower the actual monthly benefit increase to around $37.70 after premium deductions.

Additionally, more retirees are finding themselves subject to federal income taxes on their Social Security benefits.

The income thresholds that determine whether Social Security benefits are taxable have not been adjusted for inflation since 1983, meaning more retirees are now crossing those limits.

For example, single filers with combined income between $25,000 and $34,000 may pay taxes on up to 50% of their benefits, and those above $34,000 may be taxed on up to 85% of their benefits.

Looking Ahead: The Future of Social Security Benefits

Inflation has been a significant concern for retirees, particularly those on fixed incomes. Many seniors are worried that persistent high prices will deplete their savings.

According to a survey by the Senior Citizens League, 71% of seniors listed inflation as one of their top retirement concerns, with 78% reporting higher monthly budgets for essentials like housing, food, and medicine compared to last year.

The annual COLA is crucial for protecting the buying power of Social Security benefits, but some experts argue that the once-a-year adjustment may not be sufficient during periods of high inflation.

Laurence Kotlikoff, an economist at Boston University, suggests that more frequent adjustments could better protect retirees from the lag in COLA updates, which currently compensates for inflation that occurred as far back as 15 months.

Conclusion

As we await the final inflation data and the official COLA announcement for 2025, it’s clear that while any increase in Social Security benefits is welcome, retirees must also consider the impact of rising costs in other areas, such as Medicare premiums and taxes.

Staying informed about these changes is crucial for effective financial planning in retirement.

Level up casino reviews Australia edition

In this blunt review, we break down everything you should know about level up casino reviews for Australian players. Find out what matters, which platforms to consider, and pitfalls to avoid. If you’re thinking about joining or comparing online casinos, this is your guide. Get facts, not hype.

Popular Australian Casinos at a Glance

Pokies Madness: Grab 250% Up to $400 & 100 FS

Casino in Your Pocket: 110% Up to $100 & 120 Spins

Pokies Paradise: 200% Up to $2,000 + 150 Free Spins

Start Winning: 300% Bonus Up to $1000 & 75 Spins

Pay with PayID: 50% Match to $400 & 200 Free Spins

Go Big: 175% Welcome Up to $150 & 75 Spins

30% Cashback Every Week – Up to $100 Back

Jump In: 120% Bonus Up to $250 & 40 Free Spins

Aussie Players Welcome: 50% Up to $250 + 60 FS

Welcome Gift: 150% Match Up to $400 + 200 FS Included

Free Play: $100 Bonus + 15 Spins Without a Deposit

Get Started: 300% Bonus Up to $2500 + 150 Free Rounds

Intro Offer: 80% Bonus Up to $400 & 60 Free Spins

Stack the Deck: 300% Match Up to $100 & 75 Spins

Welcome Gift: 150% Match Up to $400 + 200 FS Included

Unlock 20 Free Spins on Your First Deposit

Blackjack Bonus: 80% Up to $750 on Your First Deposit

VIP Lounge Access: 175% Up to $1000 + 100 FS

Midweek Reload: 30% Bonus Up to $300 & 250 FS

High Roller Special: 175% to $3000 + 25 Free Spins

Best slot games on level up casino reviews

Online pokies and slots offer fast, exciting gameplay with instant outcomes and the possibility of sizable rewards. Below, you’ll find a curated selection of the hottest online pokies and slots trending among Australian players. Try your luck or explore new titles directly from home.

Top Online Casino Services and Games

Licensed Australian casinos deliver diverse services, from real money pokies and live-dealer games to poker tables, blackjack, and original skill-based experiences. Level up casino reviews cover which providers offer the best mix. Choose based on your preferences for big wins, variety, or strategy.

Popular Australian Casinos at a Glance

- LevelUp Casino

- Punt Casino

- National Casino

- Casino Rocket

- Fair Go Casino

- Joo Casino

- King Johnnie Casino

Top Online Casino Services and Games

- Online poker rooms

- Real money pokies

- Progressive jackpots

- Live dealer tables

- Blackjack tournaments

- Roulette games

- Baccarat and more

Best Slots and Pokies You Can Play

- Wolf Gold

- Big Bass Bonanza

- Buffalo King

- Gates of Olympus

- Starburst

- Temple Tumble

- Sweet Bonanza

- Book of Dead

- Money Train 2

- Aztec Magic

How Deposits and Withdrawals Work

Australian casino sites make depositing simple with debit cards, e-wallets, and crypto options. Withdrawals usually take from several hours up to five days, with verification needed for first-time requests. Daily and weekly withdrawal limits apply. Review each casino’s financial terms before signing up.

| Payment Method | Deposit Time | Withdrawal Speed |

|---|---|---|

| Visa/MasterCard | Instant | 1-3 days |

| Neosurf | Instant | N/A |

| Bitcoin | Instant | Within 1 day |

| Skrill | Instant | 1-2 days |

Mobile Casino Experience in Australia

Most Aussie online casinos offer sleek mobile sites or dedicated apps for Android and iOS. Features include mobile-only bonuses, quick game loading, and fast deposits. All major pokies and live games work on smartphones and tablets.

Bonuses and Promotions

Welcome packages, no deposit spins, and reload bonuses boost your bankroll. Wagering requirements typically range from 20x to 50x. Always check bonus expiry and eligible games. VIP rewards systems offer cashback, fast payouts, and event tickets for regulars.

Security and Fair Play Ensured

Look for gambling operators licensed by international authorities. All games should use RNG technology for fairness. SSL encryption protects your data. Independent audits are a positive sign. Customer funds should stay segregated from operations accounts.

Customer Support and Player Care

Quality live chat is now standard. Hotlines and email support offer extra layers. Expect a response within minutes during Aussie business hours and detailed FAQ sections for self-help. Multilingual staff are available at leading casino brands.

Responsible Gambling Tools & Advice

Responsible gaming tools include personal deposit caps, self-exclusion, and time trackers. Accredited sites promote responsible gambling organisations. Early signs of unsafe behaviour trigger notifications or account limitations. Seek help if you feel your play is out of control.

Reading the Fine Print: Terms & Conditions

Always read the small print regarding playthroughs, max withdrawal limits, and restricted games. Terms may be updated frequently. Some casinos restrict bonus play for certain games or regions. Careful reading avoids misunderstandings and disappointment.

FAQ – level up casino reviews in Australia

What is level up casino reviews?

Level up casino reviews are independent opinions, overviews, and ratings of major online casinos available in Australia, focusing on features, reliability and user experience.

Are online casinos safe for Australians?

Licensed online casinos use security protocols and fair play policies, but always check for proper regulation before playing.

Can I win real money at Australian online casinos?

Yes, you can win and withdraw real AUD winnings if you play at certified Australian-friendly sites.

Which payment methods can I use?

Common methods include Visa, MasterCard, Neosurf, cryptocurrency, bank transfer, and popular e-wallets.

What are typical bonus wagering requirements?

Most sites ask for wagering your deposit and bonus 20-50 times before withdrawal.

Is there a best time to play online pokies?

No specific time guarantees better odds, as pokies use random number generation for each spin.

Best Online Casinos in Australia 2024

Australia’s iGaming landscape is thriving with fresh brands, innovative games and player-first bonuses, making it a great time to explore top casino sites. Whether you’re into pokies, live tables or sports betting action, the following brands are popular choices among Aussie punters. Get to know which ones stand out and why.

Aussie Play Casino Experience

Aussie Play is well known for its laid-back style and huge pokies library. Players in Australia can expect a very generous welcome bonus, easy registration and local-friendly banking options. Their mobile site works fluently on even basic phones. Customer service is on hand 24/7 via live chat.

Bizzo Casino in the Australian Market

Bizzo has quickly become a favourite due to its fast payments and over 3,000 pokies from top software providers. Aussie players can use AUD for deposits and withdrawals, and weekly free spins offers help keep the excitement high. Their tournaments are a must-try for slot fans.

Caesars Casino Down Under

Caesars, an international casino giant, also accepts Australian players with a sophisticated selection of games. From classic table games to immersive live dealer experiences, it brings a slice of Las Vegas straight to your home. Advanced encryption ensures safe and private gameplay.

Casino Swish for Pokies Fans

Casino Swish makes a mark with its slick interface and huge selection of Aussie-themed pokies. Players can join loyalty programs and claim reload bonuses tailored to regular players. Its payment process is streamlined for local convenience and quick payouts.

Casinonic: Trusted Option for Australians

Australians frequently recommend Casinonic for its speedy withdrawals, secure transactions, and quality games from Pragmatic Play, Microgaming and more. Promotions are frequent and the supporting team is responsive, ensuring an easy experience for new players.

Gets Bet: Sports Betting and More

Gets Bet wraps casino, live casino and sports betting in a single platform, ideal for Aussies who like to combine pokies and wagering. Real-time odds and a seamless mobile app attract sports enthusiasts across the country.

Golden Tiger Casino’s Reputation

Golden Tiger stands out with its big progressive jackpots, frequent bonuses and a reliable Aussie support team. Its desktop and mobile sites both run smoothly, making it a long-standing favourite for Australian casino fans.

High Roller Action

If you like higher stakes, High Roller is tailored for VIP play. Its lavish perks, cashbacks and high deposit limits attract serious punters. Withdrawal times are among the fastest in the segment.

Other Noteworthy Australian Casino Sites

The following brands also have a loyal following in Australia:

- Interwetten brings strong betting options and casino games with fast pay-outs.

- Merkur features top pokies and unique branded games with easy navigation.

- Planet7Casino is famous for on-the-spot cash bonuses and round-the-clock assistance.

-

Poker Star delivers robust poker tournaments and interactive table experiences.

- Royal Ace offers both pokies and table games; attractive for both casual and experienced players.

- SlotJoint gives hundreds of pokies and flexible payment solutions for locals.

- SlottyWay is popular for its exciting slot tournaments and weekly reload bonuses.

- Sportingbet merges betting with casino action, supporting a great range of Aussie sports and slots.

- ThePokies features a local-first approach with loads of Australiana slots.

Uptown Aces and WildCardCity

Uptown Aces focuses on generous welcome bonuses, secure payment options and unique slot themes. WildCardCity is all about urban glamour with VIP privilege schemes and handy support, ensuring top rates of player satisfaction.

WynnBet

WynnBet is gaining pace with mobile-first design and exciting promotions. Its tailored sports and casino offers appeal to players who demand both action and safety.

Responsible Gambling for Australians

Before you start spinning reels or placing wagers, remember to play responsibly. Australia has support services such as Gambling Help Online and phone helplines to provide confidential advice and help you keep gaming fun and safe. Play only with money you can afford and set limits for your entertainment.

Some people who take anti-obesity medications drink less alcohol. Scientists are trying to figure out why this happens.

How Anti-Obesity Drugs Impact Alcohol Use

Anti-obesity medications, such as Wegovy and Ozempic, may lower alcohol consumption. These drugs, called GLP-1 receptor agonists, are usually prescribed to help with weight loss and type 2 diabetes. However, new research shows they might also reduce drinking habits.

A recent study found that 45% of people on these drugs drank less alcohol. The study, published in JAMA Network Open, involved over 14,000 participants. Researchers believe this connection could lead to more discoveries about these medications.

Key Findings

Here’s what the study revealed:

- Participants: Over 14,000 individuals taking anti-obesity medications.

- Results: 45% of drinkers reduced their alcohol intake.

- Drugs Used: Medications included semaglutide, tirzepatide, and liraglutide.

- Who Benefited Most: Heavy drinkers and people with severe obesity saw the biggest change.

While most participants saw no change, only 2% drank more alcohol.

Why Do These Drugs Affect Alcohol?

The exact reason remains unclear.

However, experts have a few ideas:

- Impact on the Brain: These drugs may reduce cravings by changing how the brain processes rewards. This could lower the desire for alcohol.

- Lifestyle Changes: Many people make healthier choices while on these medications, such as eating better or drinking less.

- Lower Tolerance: Weight loss reduces alcohol tolerance, which might lead people to drink less.

More research is needed to confirm these theories.

Can These Drugs Treat Addiction?

Some experts are hopeful these drugs could help with addiction in the future. However, they are not currently approved for this use.

Dr. Timothy Brennan from Mount Sinai said, “These findings are exciting, but we need more studies to understand their effects on alcohol use.”

Researchers believe these drugs have potential, but it’s too early to draw conclusions.

Should You Avoid Alcohol While Taking These Medications?

You don’t have to stop drinking completely, but experts suggest being cautious.

Here’s why:

- Side Effects: Alcohol may worsen nausea or low blood sugar, which are common side effects of these drugs.

- Calories: Alcohol contains a lot of calories, which could slow your weight-loss progress.

- Health Benefits: Reducing alcohol may improve overall health and make the medication more effective.

If you’re starting a new medication, it’s a good time to evaluate your drinking habits.

What Should You Do?

If you’re prescribed medications like Wegovy or Ozempic, consider these tips:

- Notice if your cravings for alcohol change.

- Take this chance to build healthier habits.

- Talk to your doctor if you have concerns about drinking or other side effects.

What’s Next?

The link between anti-obesity medications and reduced drinking is fascinating. Scientists need more studies to understand how these drugs work.

For now, they remain a powerful option for weight management. The added benefit of possibly reducing alcohol consumption is an exciting bonus.

Sulfur burps may be alleviated by changes in diet, proper water intake, and the use of pharmacy drugs, but it is crucial to know what causes them.

Sulfur Burps

Sulfur burps are bad-odour burps that smell like rotten eggs; many people experience this.

They can be painful and awkward and are sometimes coupled with other abdominal symptoms, including bloating, stomach-churning, or diarrhoea. The foul smell associated with sulfur burps emanates from hydrogen sulfide (H2S) generated inside your stomach.

To know how to treat and get rid of sulfur burps, it is essential to understand the causes that contribute to it.

This article will look at possible causes of sulfur burps, options for natural cure remedies, medical treatment, and ways of avoiding them.

What Causes Sulfur Burps?

Sulfur burps occur when hydrogen sulfide gas builds up in the stomach and is released through burping.

Various factors can contribute to the production of this gas, but here are the most common causes:

- Dietary Choices

Certain foods high in sulfur content can contribute to the production of sulfur gas. Some of these foods include:- Eggs

- Meat (especially red meat)

- Cruciferous vegetables like broccoli, cabbage, and cauliflower

- Garlic and onions

- Dairy products

- Beans and legumes

- Gastrointestinal Infections

Some infections, particularly those caused by bacteria like Helicobacter pylori or parasites like Giardia, can lead to sulfur burps. These infections can disrupt your digestive system, leading to excess gas production. - Indigestion or GERD (Gastroesophageal Reflux Disease)

Indigestion or GERD can slow digestion, allowing food to sit in the stomach longer and produce more gas. This gas can sometimes have a sulfurous smell, leading to sulfur burps. - Food Intolerances

Lactose intolerance, gluten sensitivity, or other food intolerances can cause incomplete digestion of food, leading to gas buildup and sulfur burps. - Medications

Some medications, particularly those containing sulfur compounds or antibiotics that affect the balance of gut bacteria, can contribute to sulfur burps.

Natural Remedies to Get Rid of Sulfur Burps

Although passing sulfur burps might be embarrassing, in most cases, they can be cured naturally. Below, I give you some home remedies that may help if you decide to try:

1. Stay Hydrated

Proper digestion requires that one drink enough water, which is determined by the intensity of the exercises. Drinking fluids eliminates accumulated toxins, thus ensuring the digestive system is working properly, and there is less likelihood of developing gas. Avoid sulfur burps by taking at least eight glasses of water per day.

2. Green Tea or Herbal Teas

Green tea, mint, or chamomile will also relax your tummy and reduce gas formation. Green tea, in particular, has antioxidants that can help with digestion, while peppermint helps to relax the gut.

3. Eat Smaller, More Frequent Meals

Eating large meals or taking more than necessary also puts pressure on the digestive system, resulting in information of gases, including sulfur. Dividing the portions into smaller meals that are taken frequently ensures that the body can break down the food into Sulphur without experiencing sulfur burps.

4. Avoid Sulfur-Rich Foods

If you experience sulfur burps often, you should reduce the intake of sulfur-containing foods such as eggs, broccoli, garlic, and dairy products. These foods may cause more gas production; therefore, cutting down or eliminating these foods from the diet may greatly help.

5. Try Apple Cider Vinegar

Apple cider vinegar (ACV) is one of the go-to home remedies for enhancing digestion. ACV has an impact on balancing the level of acidity in the stomach, hence facilitating the digestion of foods and decreasing the formation of sulfur gas. Ingest a glass of water mixed with 1 tablespoon of ACV, and see if it is taken before meals.

6. Use Probiotics

Probiotics are beneficial bacteria that promote healthy digestion by balancing the gut’s bacterial environment. Taking a probiotic supplement or eating probiotic-rich foods like yogurt, kefir, or sauerkraut can help prevent sulfur burps by keeping your digestive system balanced.

Over-the-Counter Remedies for Sulfur Burps

Several over-the-counter treatments are available if natural remedies aren’t enough to resolve your sulfur burps.

1. Antacids

Many recipes warn about foods that produce gas, but antacids can help neutralize stomach acid and leave your digestive system to do the work. This may be useful, especially if the sulfur burps originate from indigestion or GERD.

Table: Best OTC Medications for Sulfur Burps

| Medication Type | How It Helps | Example Products |

|---|---|---|

| Antacids | Neutralize stomach acid | Tums, Rolaids |

| Simethicone | Breaks up gas bubbles in the stomach | Gas-X, Mylanta Gas |

| Probiotics | Supports gut health | Culturelle, Align, Florastor |

2. Simethicone

It is an anti-gas drug that alters the sizes and distribution of gas in the stomach and intestines, promoting gas release without the smell.

Simethicone-containing products such as Gas-X or Mylanta Gas quickly relieve such pain.

3. Activated Charcoal

Charcoal is effective in absorbing gases and toxins in your stomach. The common formulation is a pill that can successfully minimize normal gas and sulfur-related burps.

Always check with your doctor before using charcoal supplements, as they may interfere with medications.

When to See a Doctor for Sulfur Burps

While sulfur burps are often harmless, they can sometimes signal an underlying health issue that requires medical attention.

If your sulfur burps are persistent or accompanied by other symptoms, such as severe abdominal pain, diarrhoea, nausea, or vomiting, it’s time to consult a doctor.

Here are a few conditions that may require medical evaluation:

1. Gastrointestinal Infections

As mentioned earlier, infections like H. pylori or Giardia can cause sulfur burps and other symptoms like bloating, nausea, diarrhoea, and stomach cramps. Testing for these conditions often involves stool, blood, or breath tests.

2. GERD or Chronic Indigestion

GERD or chronic indigestion can lead to frequent sulfur burps due to slowed digestion. If you experience heartburn, regurgitation, or pain after eating, consult a healthcare provider for proper diagnosis and treatment.

3. Food Intolerances or Sensitivities

Food intolerances, such as lactose intolerance or celiac disease, may cause sulfur burps. Your doctor may recommend elimination diets or tests to identify specific food triggers.

Prevention Tips: How to Stop Sulfur Burps from Coming Back

Once you’ve gotten rid of sulfur burps, preventing them from returning is essential. Here are some long-term strategies you can follow:

1. Monitor Your Diet

Pay attention to how certain foods affect your digestive system. Keeping a food diary can help you identify which foods trigger your sulfur burps so that you can adjust your diet accordingly.

2. Eat Slowly and Chew Thoroughly

Eating too quickly can cause you to swallow air, leading to gas and burping. Chewing food thoroughly helps your digestive system break down food more efficiently, reducing the chance of sulfur gas forming.

3. Avoid Carbonated Beverages

Carbonated drinks like soda and sparkling water introduce extra air into your stomach, which can lead to burping. Try to cut down on these beverages to reduce gas and sulfur burps.

4. Exercise Regularly

Regular physical activity can improve digestion by keeping things moving through your gastrointestinal tract. Even light activities like walking after a meal can help prevent gas buildup.

5. Stay Hydrated

Hydration is vital to maintaining healthy digestion. Water helps break down food and keeps things moving through your digestive system, reducing the likelihood of gas formation.

Banish Sulfur Burps for Good

Sulfur burps may be unpleasant, but they’re usually treatable with dietary changes, natural remedies, and over-the-counter medications.

Whether you’re dealing with a one-time issue or chronic sulfur burps, identifying the underlying cause is the first step toward relief.

By adjusting your diet, staying hydrated, and trying some of the remedies outlined here, you can eliminate sulfur burps and prevent them from returning.

Remember, if sulfur burps persist or are accompanied by other severe symptoms, it’s essential to consult a healthcare provider to rule out any underlying health issues.

iOS 26 Explained: Stability & The Future of iPhones

Level up casino reviews Australia edition

Magnitude 5.1 Earthquake Rattles Northern Iran — No Major Damage Reported

-

FASHION9 years ago

FASHION9 years agoThese ’90s fashion trends are making a comeback in 2017

-

Entertainment9 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

FASHION9 years ago

According to Dior Couture, this taboo fashion accessory is back

-

Sports9 years ago

Boxing continues to knock itself out with bewildering, incorrect decisions

-

Entertainment9 years ago

Disney’s live-action Aladdin finally finds its stars

-

Sports9 years ago

Phillies’ Aaron Altherr makes mind-boggling barehanded play

-

Entertainment9 years ago

The old and New Edition cast comes together to perform

-

Entertainment9 years ago

Mod turns ‘Counter-Strike’ into a ‘Tekken’ clone with fighting chickens